;window.open('https://pinterest.com/pin/create/button/?url=https%3A%2F%2Fmango.bz%2Fnews%2Fclub-thrifty-how-to-budget-a-personal-budget-guide-that-actually-works-1498&media=https://mango.bz/assets/mango/images/news.jpeg&description=News+-+Club+Thrifty+%2F+How+to+Budget%3A+A+Personal+Budget+Guide+That+Actually+Works+-+Mango+Publishing', '', 'height=300, width=600');){kind=link}

Posted by Greg Johnson

Budgeting.

It seem so restrictive. It seems so impossible. It seems so…yuck, right?

Stick with me here.

Learning how to budget may seem like a daunting task…but it doesn’t have to be! Creating a budget that actually works is a relatively simple process that can change your financial life forever.

Maybe you’ve tried budgeting before and failed. Maybe you’ve wanted to save money, but you just don’t know how. Or, maybe you’re sick and tired of living paycheck to paycheck, spending all you earn and digging yourself deeper into debt with each passing day.

Trust me, I know how it feels.

I’ve been there before. I’ve struggled. I’ve been in debt.

But since I’ve learned how to budget, I’ve never had to worry about money ever again.

Table of Contents [show]

You Are Not Alone

If you’ve been struggling with money, chances are that you’ve searched high and low for quick tricks and easy cures to cure your money woes. You’re not alone. Most of us have.

We’ve tried making extra money from home. We’ve clipped coupons, shopped sales, and used all of those “expert” tips with few results. Years of financial struggles and budget failures have crushed our money dreams…

Today, is the day we turn that all around!

You see, the solution has always been right in front of us, and we’re going to unlock that path together! It actually quite simple once you get the hang of it. In fact, I believe it could change your life. Heck, it changed mine.

Here’s the secret: You need to create a budget that actually works. It sounds difficult, right? Trust me, it’s not.

Today, you’re finally going learn how to budget in an easy, realistic way that will ease your financial pain and set you on the path to financial freedom. This budgeting process will help you manage your money properly so you’re not stuck scrambling at the end of every month. It’s a simple formula that anybody can execute and use to succeed.

So, wherever you are on your financial journey, you’ve come to the right place. We’re super excited you’re here.

Let’s get started, shall we?!?

Will a Monthly Budget Really Work?

Are you deep in debt and are desperate to find a way out? This guide will work for you.

Do you a make a six-figure income but can’t figure out where all your money is going? This is the budgeting guide for you!

Do you fall somewhere in between? Then this guide is for you.

Learning how to budget your money is the most important financial skill you can master. Best of all, anybody can do it!

All I ask from you is this:

- Follow the steps provided.

- Try your best.

- Be honest with yourself.

If you can do these three things, I promise that you WILL see positive results!

Why Should I Learn How to Budget?

Why does anybody need to create a budget? Here’s why:

- It gives you a clear, visual picture of where finances sit each month.

- It helps you to save money on the things that don’t matter so you can spend on the things that do.

- It teaches you financial discipline.

- Rather than making assumptions about how good (or bad) you are doing, budgeting requires you to face the actual facts of your financial situation.

- A budget creates a plan that dictates how your money will work for you.

- You will start to “find” money you didn’t know you had (or that you were spending).

- You will learn how to live within your means.

- You will be able to track and see the results.

- Most importantly, it gives you control over your money and your life.

What is a Personal Budget?

Now that we know why a monthly budget is important, let’s talk a little bit about what a budget actually is.

A lot of people are scared off by budgeting because they think it’s too restrictive. They cling to the notion that starting a budget means they’ll never be able to buy what they want EVER AGAIN.

In reality, this couldn’t be further from the truth.

Your monthly budget will help you get more of what you truly want, not less.

A personal budget is a monthly financial plan for both your income and your spending. Basically, a budget helps us decide what we are going to do with the money we make each month. It helps us save money on the things that don’t matter so we have more to spend on the things that do.

It’s really as simple as that.

Budgeting Tools: What You Need to Get Started

The great thing about making a budget is that it doesn’t take a lot of equipment to get started.

All you need is a simple pen and paper.

Yep. That’s it.

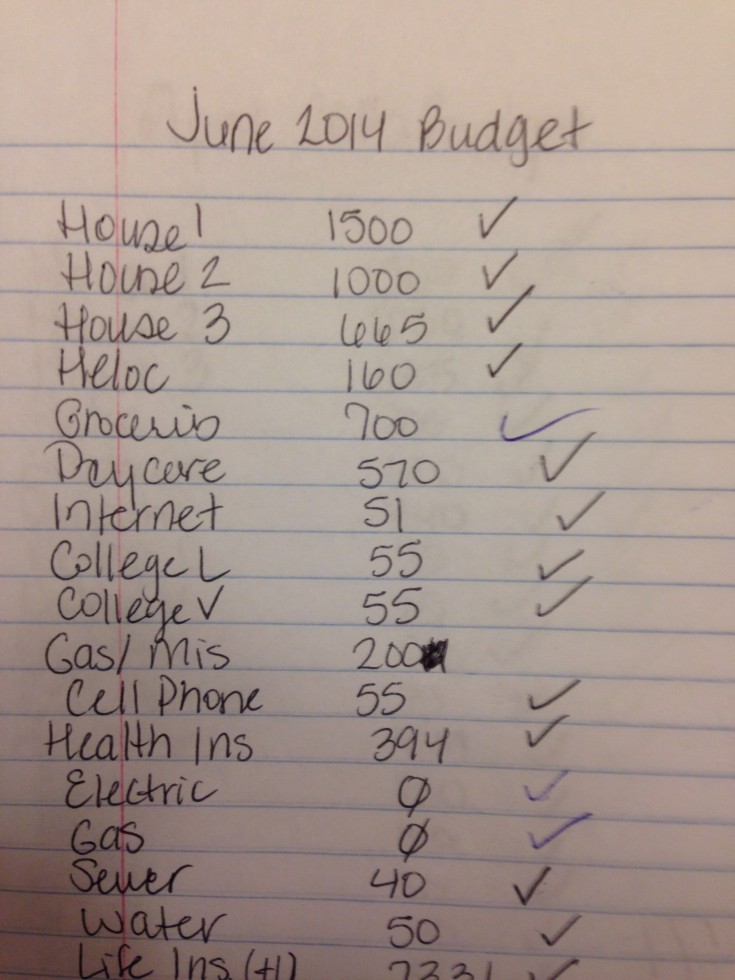

Sure, there are some really great financial tools and budgeting apps available (follow the link to find our top 10!). With that said, Holly and I still use a paper and pen to this day!

Each month, we get out our spiral bound notebook, think about the month’s expenses and income, and get to work jotting it down. It only takes about 10 to 15 minutes, but it is the most important money discussion that we have each month.

Just to prove how long we’ve been doing it this way, here’s a quick peek at a (really) old budget of ours.

It’s not fancy, but it works.

Notice that I said we do this every month. Why? Because it’s that important.

A budget is a living, breathing document. You have to create a new one for every month.

Each time the calendar rolls over, you’ll have different expenses to account for. Your budget needs to reflect this, so it is uber important that you update it every month.

So, let’s grab that pen and paper and get to work!

How to Make a Budget in 6 Easy Steps

Zero-Based Budgeting: Zero is the Goal

What you are about to learn is called a zero-based budgeting, sometimes referred to as a zero-sum budget.

The goal of a zero-based budget is to ensure that your income and expenses are exactly balanced (“zeroed out”). You’ll do this on a monthly basis by giving every single dollar that you make a specific purpose.

This is so important I’m gonna use some fancy bold and italics to drive home my point.

Your income and your expenses should balance to the penny!

You’re not rounding to the nearest $5. You’re not guessing that you’re gonna save about $200 this month. You are going to be specific. You are going to be exact. You are going give each and every dollar a job, tell it where to go, and take control of your financial life. You are in charge of your money, not the other way around.

Budgeting is about details. If you take care of your pennies, you’ll never have to worry about your dollars again!

Here’s the simple formula you’ll use to balance your new monthly budget:

Income-Expenses-Savings=Zero

Easy peasy, right? OK, let’s get started.

Step 1: Write it Down

The first step may be the most crucial step of all. In order to create a budget that works, you need to write it down.

Let me repeat that: You need to write your budget down.

It can’t be in your head. Keeping it there is a recipe for mistakes.

It can’t be a guess. Guessing leaves too much room for error.

You need to be exact.

Your budget must be written down, clearly, so you can see it.

Now, writing it down can mean many things. You can write it down on a sheet of paper, like we do. You can use a nifty little spreadsheet (which you can get by clicking below). Or, you’re feeling super fancy, you can even use an online app like Tiller to help you budget.

It doesn’t matter how you write it down. What matters is that it is written down somewhere where you can physically see it…with your eyes!

See Also: How to Make a Budget in Excel

Step 2: Determine Your Income

If you’re like most people, your income varies slightly from month to month. However, you want your numbers to be as exact as possible. Rather than estimate your future earnings, try using actual earnings instead!

Eventually, you want to get far enough ahead that you can use last month’s income to pay this month’s bills. This is by far the most accurate way to budget. It’s also going to help break the cycle of living paycheck to paycheck.

If you don’t have enough saved to make this happen, don’t panic. But, don’t pull a number out of thin air either. Simply use your last paycheck as the basis for that month’s earnings.

Now, if you’re really strapped, you may need to get a little creative at first – especially if you get paid twice a month. If needed, adjust your budget so that you’re creating a separate budget for each paycheck.

For instance, all of your bills due between the 1st-15th should come out of the paycheck you receive on the 1st. All expenses due between the 16-31 should come out of the paycheck you receive on the 15th.

If you want to simplify things even further, contact your billing companies so that your expenses are equally distributed across your paychecks.

Again, this isn’t ideal, but it can help you get started. After a few month’s, you should have enough saved to start paying this month’s bills with last month’s income.

Hot Tip: Create your budget immediately after getting paid. This will make it super simple for you to figure out how much money you have to spend.

So, at the top of your budget, go ahead and create a category for income. Add up all the money you made the previous month (or what you will make for the current month), and jot the number down there. Draw a line underneath it and move on to the next category.

Step 3: Pay Yourself First

Immediately below your income category, create your first expense category: Savings.

Yep, I want you to think of your savings as your very first – and most important – expense.

Before you even think about paying anybody else, try paying yourself first. This is going to help place your focus where it needs to be – on saving rather than spending.

If you don’t have an emergency fund, this is where you should start building one. (Saving 10% of your take home pay until you have at least $1,000 is a good place to start.) Here is where you’ll eventually fund cash savings, additional retirement accounts (like your Roth IRA), and college savings plans as well.

Quick! Do it now before you calculate your expenses.

Paying yourself first can help you save more than you ever thought possible!

Step 4: Determine That Month’s Expenses

Alright, now it’s time to determine your expenses. Place this section directly below the savings section on your budget worksheet.

First, break your expenses down into two categories: fixed and variable.

Generally, your fixed expenses are those that stay the same each month. Fixed expenses may include:

- Mortgage or rent

- Health insurance premiums

- Life insurance premiums

- Cable

- Internet

- Phone

- Cell phone

- Student loan repayment

- Car payment

It’s important to understand that “fixed” expenses aren’t always necessary expenses. Expenses like cable TV and your cell phone bill are optional expenses. Nevertheless, “fixed” means that they don’t change from month to month.

Next, you’ll list variable expenses like:

- Utilities

- Groceries

- Entertainment

- Restaurant spending

- Clothing

- Miscellaneous

Unfortunately, you’ll need to estimate these expenses on a month-to-month basis or as the need arises. Using last month’s bill tends to help you be as accurate as possible.

When estimating variable expenses, be sure to leave a buffer! You always want to estimate a little bit high so you’re not scrambling to come up with the money later.

Remember, also, that every expense for the month must fit into one of these categories. Every single penny you spend (and earn) must be accounted for!

Step 5: Review and Balance

Good job! You’ve created all of your budget categories…but you’re not done yet.

Now that the hard work is done, you need to make sure that your budget is balanced. Remember, with zero-based budgeting, the goal is to “spend” every penny you make into your budget categories. Here’s the formula once again in case you forgot it:

Income-Savings-Expenses=Zero

What to Do if You Have a Negative Number – If your equation balances to a negative number, you have overspent. You’ll need to make adjustments by cutting your expenses (preferable), cutting your savings (not preferable), or increasing your income by the amount you are negative. Once you’ve made the necessary adjustments, go back and run the equation again.

What to Do if You Have a Positive Number – If your equation balances to a positive number, congratulations! You have extra money in your budget!!! Quick, go stash that money in your savings account before you’re tempted to spend it.

Step 6: Repeat Each Month

Huzzah! You’ve just completed your first monthly budget. Congratulations!!!

Now that you’ve got the template down pat, it will be even easier for you to complete it next month.

If your budget fell apart this month, don’t worry. We’ve all failed with our budget at one point or another, and it usually takes some practice to get it right.

The important thing is that you have the tools now to make it work. Keep at it, and you’ll work out the kinks in no time.

Budgeting Tips and Tricks

As I mentioned before, all of us have failed with our budget at one time or another. Even me.

It might take some time, but even you can learn how to stick to a budget. Here are some tips and tricks to help you get there.

- Write it Down – If you remember nothing else from this piece, remember this: Write. It. Down.

- Automate Your Savings – Think of your savings as an expense, your most important expense, and pay yourself first. You can even have the amount you want to save automatically deducted from your paycheck. Just have it directly deposited into an online savings account, and you’ll see an instant difference.

- Reward Yourself – When you reach certain savings goals, give yourself a pat on the back. It is OK to treat yourself sometimes, provided you plan for it in your budget.

- Be Kind to Yourself – If you go over budget, don’t beat yourself up. This is a marathon, not a sprint. Analyze where your mistakes were made, fix them, and give it your best shot next month.

- Be Honest and Realistic – Don’t fudge on your budget by underestimating or guessing at expenses. This will not work. Whenever possible, be exact. When it’s not, leave a cushion by slightly overestimating your expenses. Be honest about where your money is going, use realistic numbers, and you will see results.

Budget Accessories

Creating a budget that works is just one of the tools you should have in your financial toolbox. Here are a few more accessories to consider that will help you make the most of your money.

Expense Tracking

Now that you have a monthly budget, you need to make sure it works! Tracking your spending does just that. By tracking your spending, you’ll be able spot any holes in your budget, identify areas where you are overspending, and make budgeting adjustments as needed. Learn how to track your spending here.

Emergency Fund

The most common cause of failed budgets are unexpected expenses. Unfortunately, these are bound to happen. The only thing you can do is make sure that you’re prepared. That’s why having an emergency fund is so important. An eFund helps you weather the storm and keeps your budget on track. By having money tucked away for emergencies, you can ride out any issues without destroying your savings goals. Learn how to start an emergency fund here.

Free Money Tools

Personal Capital, has some great money tools and they are totally FREE! Try using their “cash flow tool” to automatically track your expenses and help you stick to a budget. They also have a free retirement calculator, an investment fee analyzer, a net worth tracker and more. Check out our complete Personal Capital review to learn more.

Wrapping It Up

There it is! Now, you know how to make a budget that really works. By following these steps, you’re well on your way to seizing control of your financial life!

For us, taking control of our money meant that we were able to get out of debt. That led to us quitting our jobs, starting our own business, and traveling the world! Who knows where budgeting might lead you!

To control your life, you must be in control of your money… and that begins with your budget. Now get after it, and start your first budget today!